Costa Rica: As of January 1996, the 70 percent of Mexican agricultural exports to Costa Rica are duty -free.

|

NAFTA has proved is worth in good times and bad. Following an exceptionally good year in 1994 for inter-NAFTA trade, NAFTA in 1995 helped Mexico weather the storm of the economic crisis, while it diminished its impact on trading partners. For example, while U.S. exports to Mexico fell by two percent, Mexican imports from the European Union fell 25 percent.

Also, in only two years the average U.S. custom tariff on Mexican products has dropped from around four percent to 1.5 percent, while the average duty Mexico applies to U.S. products has fallen from 10 percent to 4.9 percent.

As Mexico's economy returns to positive growth in 1996, Mexico's imports from its NAFTA partners will recover and exports will continue their strong performance.

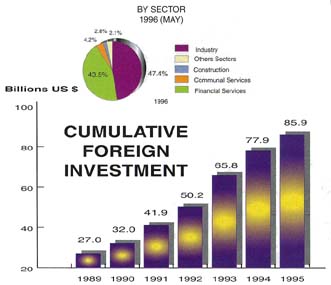

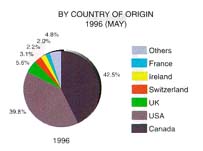

Since NAFTA entered in force, total foreign direct investment into Mexico reached $US16.5 billion dollars (January 1994-April 1996). U.S. and Canadian investments account for almost 60 percent of this amount. In 1995 alone, $US5.5 billion in foreign direct investment materialized in Mexico. Most of this new investment was directed to the manufacturing sector.

Chile: This agreement came into effect on January 1, 1992. And since the first of 1996 the custom duty will be eliminated on 97 percent, to be completely erased by 1998.

|

Colombia and Venezuela: Known as the G-3 agreement, the accord will allow Mexican exports into a market that is worth over US$20 billion.

Costa Rica: As of January 1996, the 70 percent of Mexican agricultural exports to Costa Rica are duty -free. |

|

|

Bolivia: The agreement went into effect on January 1, 1995. Since then, 97 percent of Mexican exports to Bolivia have become duty free.

Bilateral Investment Agreements: Mexico signed these agreements with Spain and similar ones with Switzerland. Mexico has also begun negotiations with the Netherlands, France and Germany. Informal proposals have been exchanged with the UK and Italy. |

|